3

关注

226

关注者

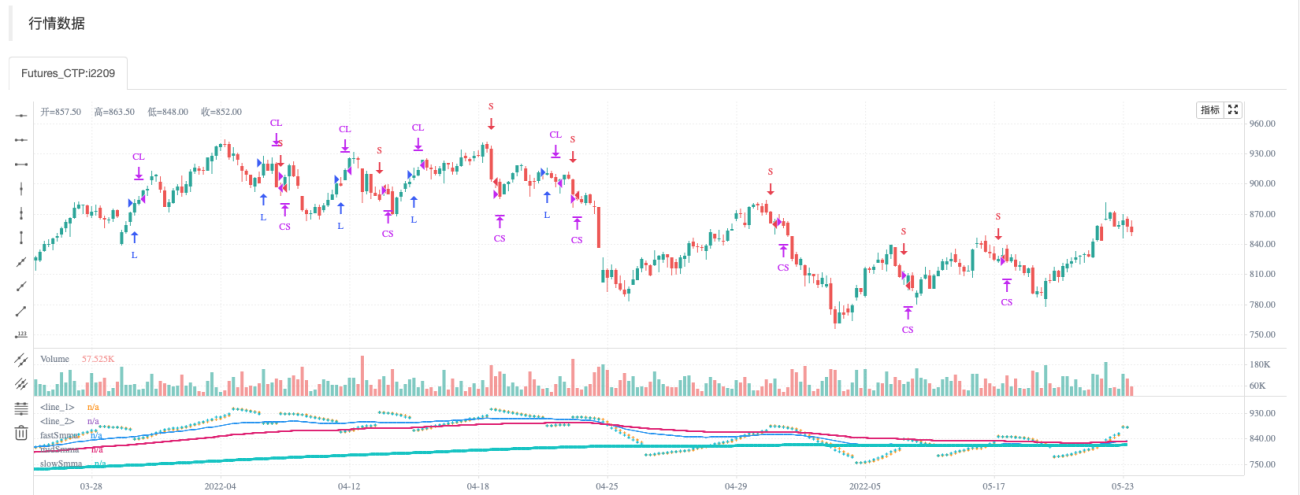

此脚本是SAR策略和3个平滑移动平均值的组合。

策略:

当所有3个SMMA都上升时,需要SAR多头。当所有3个SMMA都下降时,做空SAR。支持StopLoss和TakeProfit。

回测测试

策略源码

Pine

/*backtest

start: 2021-12-01 00:00:00

end: 2022-05-24 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_CTP","currency":"FUTURES"}]

args: [["ContractType","i2209",360008]]

*/

//@version=5

//strategy(title="SAR + 3SMMA with SL & TP", overlay=true, calc_on_order_fills=false, calc_on_every_tick=false, default_qty_type=strategy.percent_of_equity, default_qty_value=100, currency=currency.USD, commission_type= strategy.commission.percent, commission_value=0.03)

start = input.float(0.02, step=0.01, group="SAR", title="开始")策略参数

评论

全部评论 (0)

暂无数据

- 1