3

关注

226

关注者

基本原理

该指标背后的基本原理是:当资产价格达到极限时,无论趋势如何,都会出现(可能不相等,但)相反的反应。

设置

无论您选择什么时间段,默认设置都不是最好的。我个人认为,JMA的长度最好比“正常”长。

JMA来源:Jurik移动平均线计算基于的来源。

JMA长度:控制Jurik移动平均线的长度。

JMA阶段:各种各样的滞后控制器。增加相位会增加过冲,但会减少滞后,减少相位会减少过冲,但会增加滞后。

ATR长度:计算平均真实范围值的长度。

ATR乘数:该乘数控制信封或极端频带的“宽度”。

学分

@gorx1用于改进和更精确(?)Jurik移动平均值计算。

@用于ATR包络计算的redktrader。

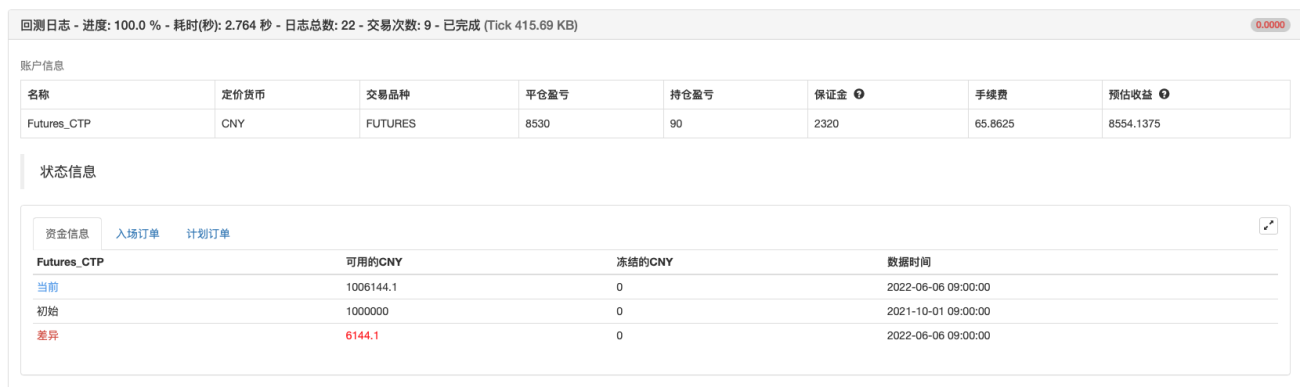

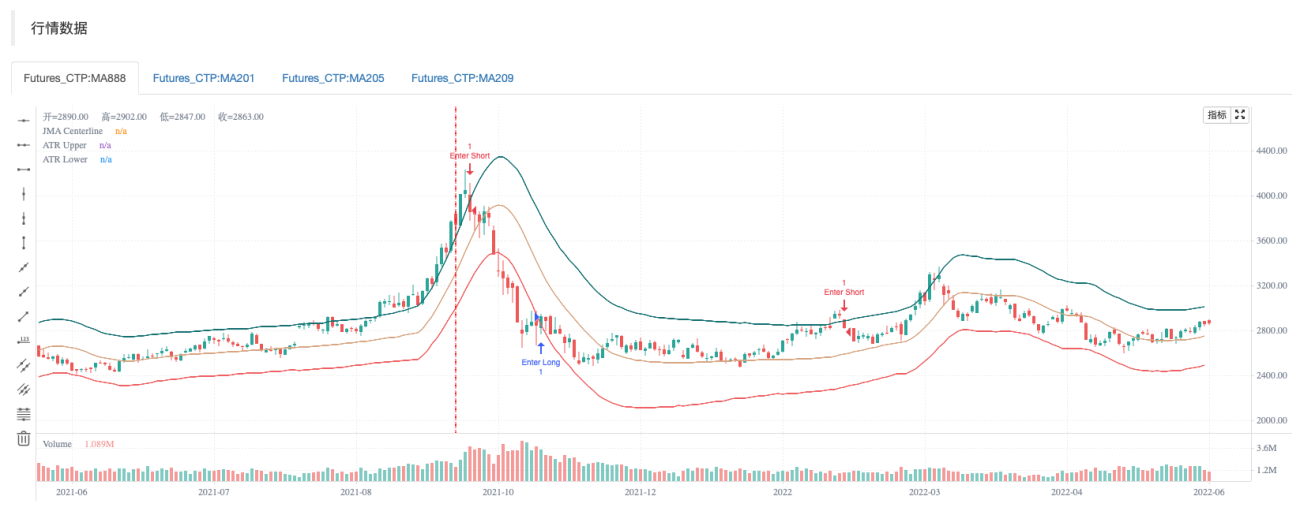

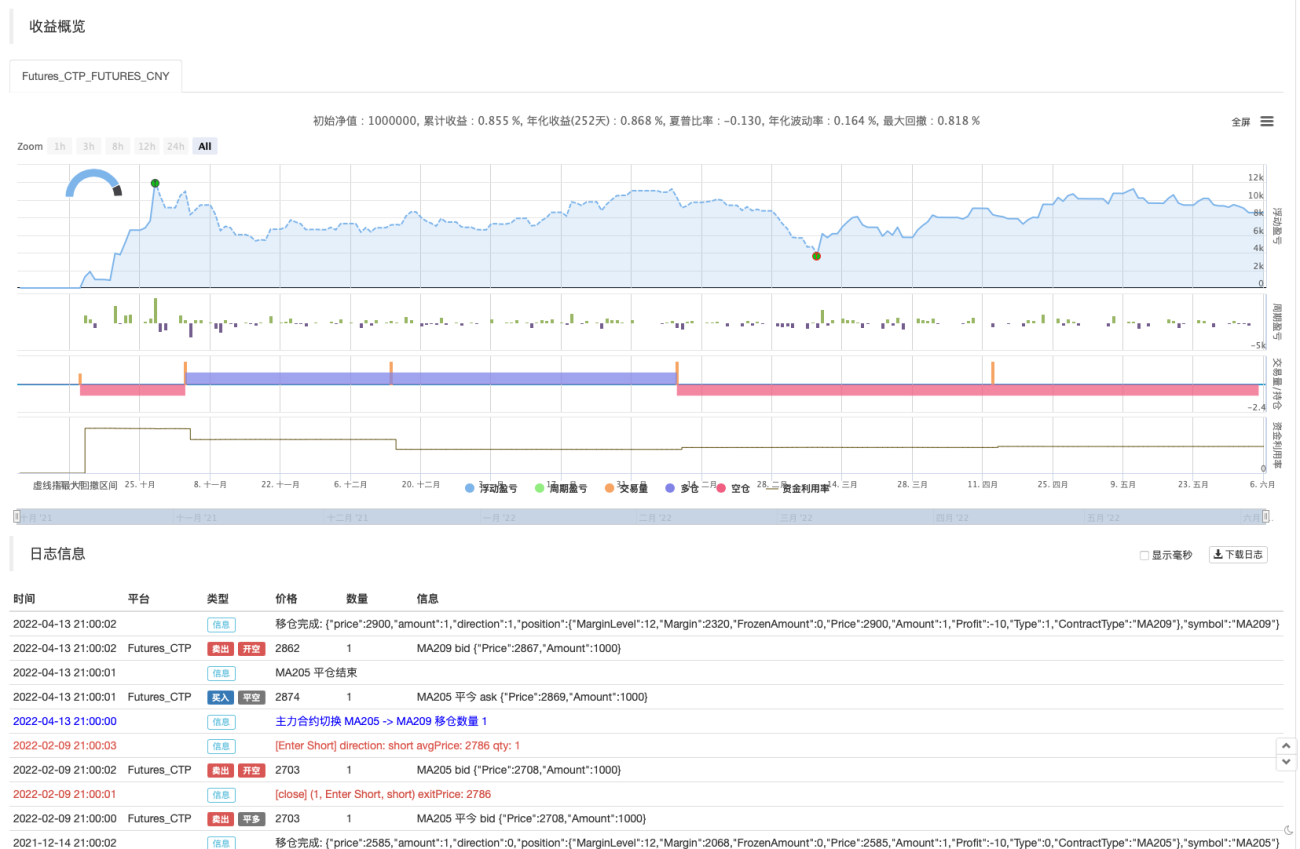

回测测试

策略源码

Pine

策略参数

评论

全部评论 (0)

暂无数据

- 1