3

关注

226

关注者

该策略使用CCI+2 RSI+2 EMA生成交易信号。交易仅在正常交易日进行,所有未平仓交易均在当前交易日结束前15分钟关闭。使用尾部止损,并且可以自定义。

非交易建议,使用风险自负。

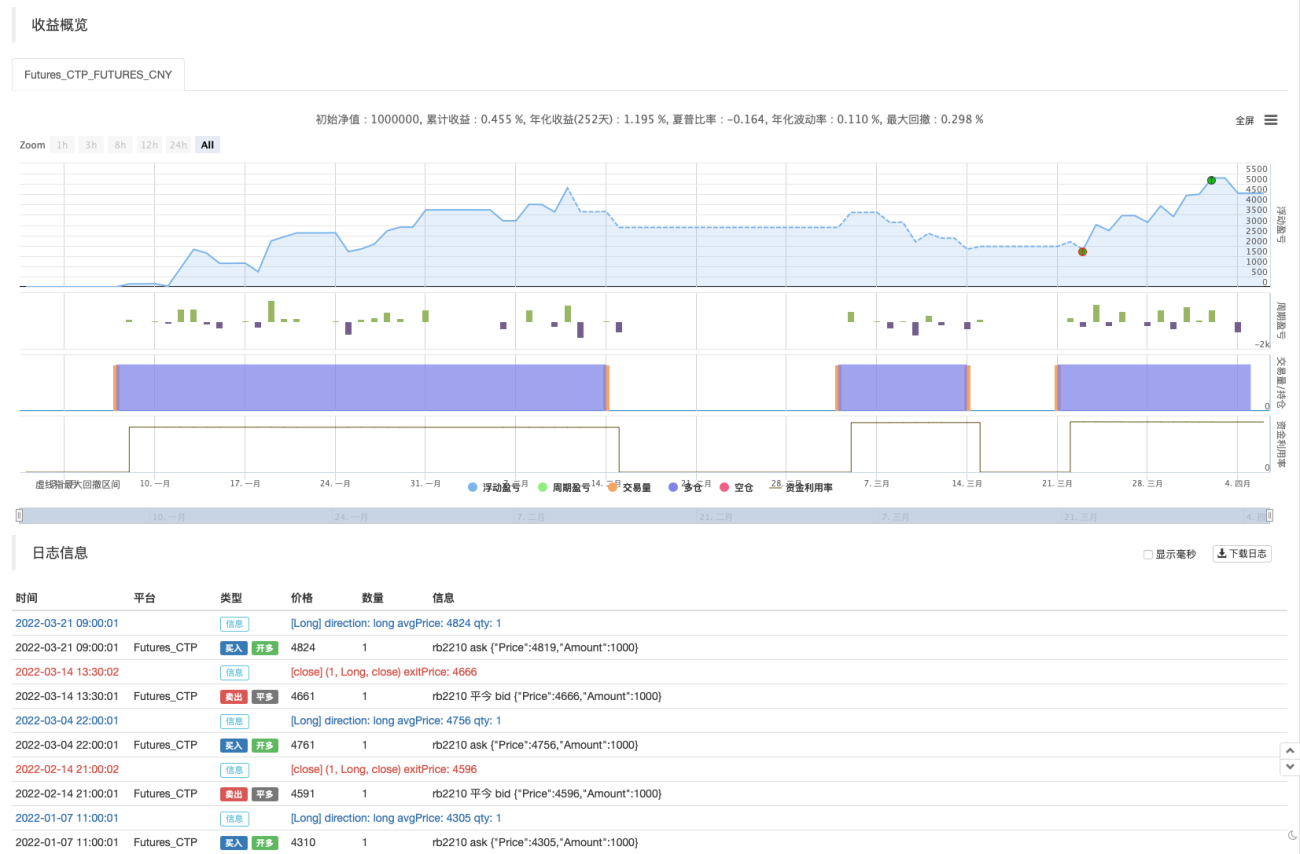

回测测试

策略源码

Pine

/*backtest

start: 2022-01-01 00:00:00

end: 2022-04-06 23:59:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_CTP","currency":"FUTURES"}]

args: [["ContractType","rb2210",360008]]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © rwestbrookjr

策略参数

相关策略

评论

全部评论 (0)

暂无数据

- 1