3

关注

226

关注者

我花了很多时间寻找最佳的基于动量的指示信号。所有人的困难在于,他们总是在一些预定义的规则上下注,这些规则可以识别或确认轴心点。通常是时间因素——在特定数量的蜡烛之后,确定轴心点。当市场运行相对缓慢时,这种方法可能是最好的,但当价格开始上下波动时,就不可能准确地遵循之字形。另一方面,如果设置得太紧(例如,仅在2根甚至1根蜡烛后确认枢轴),则会得到数百条锯齿线,它们不会告诉您任何信息。

我的观点是跟随市场。如果已反转,则已反转,无需等待预定义数量的蜡烛进行确认。在动量指标(如最受欢迎的MACD)上,这种逆转总是显而易见的。但一条单行移动平均线也足以引起反转。或者是我最喜欢的一个——QQE,我从JustUncleL那里借来(并改进了),JustUncleL从Glaz那里借来,Glaz从。。。我甚至不知道定量定性估计的来源。感谢所有这些人的投入和代码。

因此,无论你选择哪种动量指标——是的,都有一个“选择你的毒药类型”选择器,就像著名的移动平均线指标一样——一旦它反转,就会捕捉到冲动的最高点(或最低点),并打印出“ZigZag”。

有一件事我需要强调。此指示器不重新绘制。这可能看起来有点延迟,尤其是与TradingView上的所有其他曲折指标相比,但事实上是这样的。这其中有一个价值——我的指示器在被注意到的那一刻准确地打印轴心点和之字形,而不是更早地假装速度比实际速度快。

作为奖励,该指标标记了哪种冲动具有力量。很高兴看到一种前进的冲动,但没有力量——很可能会发生更大的逆转。

我将发布更多基于此之字形算法的脚本,所以请在TradingView上关注我以获得通知。

享受

回测测试

策略源码

Pine

/*backtest

start: 2021-02-01 09:00:00

end: 2022-05-22 15:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_CTP","currency":"FUTURES"}]

args: [["ContractType","i888",360008]]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © Peter_O

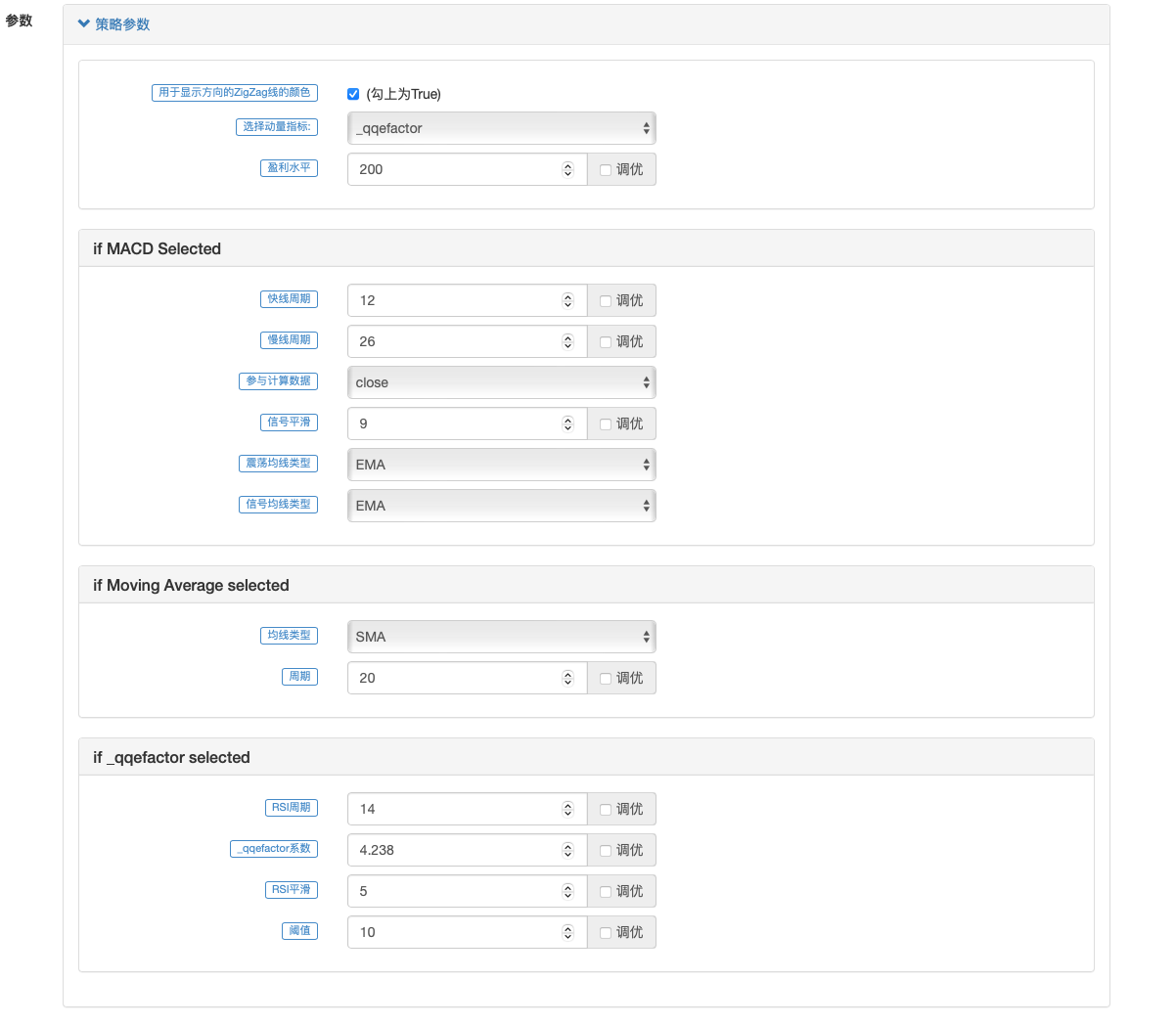

策略参数

评论

全部评论 (0)

暂无数据

- 1