3

关注

225

关注者

Stochastics Oscillator指标设置为:5,3,3

等级 : 15, 85, 30, 70

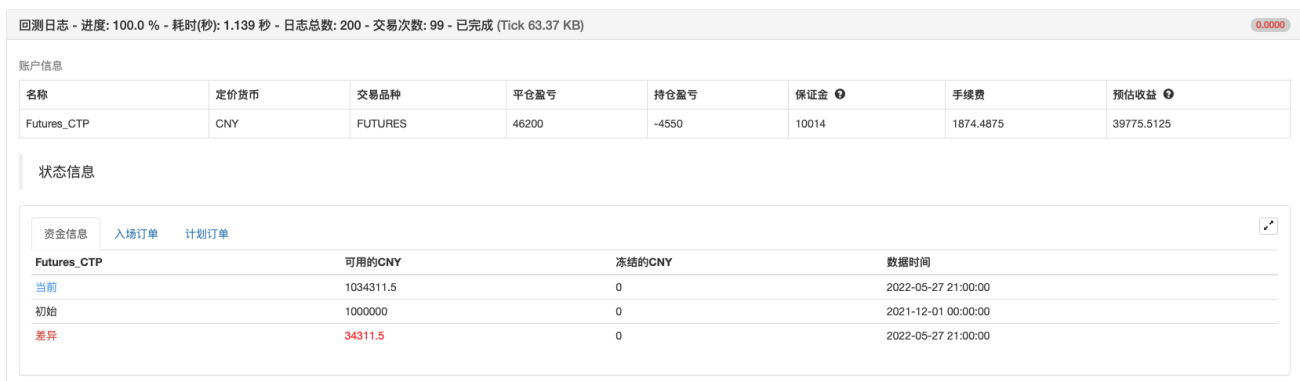

回测测试

策略源码

Pine

/*backtest

start: 2021-12-01 00:00:00

end: 2022-05-30 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_CTP","currency":"FUTURES"}]

args: [["v_input_int_1",15],["v_input_int_4",9],["v_input_int_5",2],["v_input_int_6",2],["ContractType","i2209",360008]]

*/

//@version=5

indicator('Nik Stoch')

lookback_period = input.int(15, minval=1, title="回看周期")策略参数

评论

全部评论 (0)

暂无数据

- 1